The Middle Corridor's Moment: Risks, Alternatives and the Limits of Opportunity

Elene Chkhaidze

Key Takeaways:

Reliability is the new currency of connectivity. Geopolitical volatility in Ukraine and the Red Sea has repositioned reliability as the primary driver of transit demand. Future corridor viability will be determined less by geography and more by predictable customs coordination and favorable insurance premiums.

The Caucasus sits at the centre of geopolitics, but not always at the centre of decision-making. Only specific routes, such as the Middle Corridor and one branch of the INSTC, transit the region, while others, like Iran's new southern land corridor, are engineered to bypass it entirely.

The Middle Corridor's window of opportunity is time-bound. Its ability to attract flows depends on the continued political risk of Northern and maritime routes, but capturing this shift requires addressing port bottlenecks and formal border barriers in the Caspian and Caucasus.

The Zangezur/TRIPP Corridor remains a conditional prospect. While it could compress China-Europe transit times, its realisation depends on navigating real-world hurdles: financing, regulatory approvals, and sustained political consent from Armenia.

Regional relevance hinges on concrete policy choices. Whether Armenia, Azerbaijan, and Georgia become central nodes depends on their ability to move beyond zero-sum "corridor competition" and invest in the infrastructure and coordination required for a stable transit environment.

Background

Economic corridors are becoming more important as global trade networks grow more interconnected. While geography still matters, it no longer guarantees success. Instead, corridors are shaped by practical challenges like funding, governance, sanctions risk, insurance costs, and capacity. Many countries aim to profit as logistics hubs, but success depends on how effectively they overcome existing hurdles.

The war in Ukraine, now in its fifth year, has fundamentally accelerated these dynamics. The conflict remains in a state of high-intensity stalemate, effectively rewriting the rules of Eurasian trade in real time. For the business world, the result is one of long-term strategic fragmentation. Since the 2022 invasion, over 1,000 businesses have withdrawn from Russia. While future political settlements could theoretically alter the landscape, the Northern route's persistent risk profile remains defined by strict compliance regulations. As Russia diversifies its methods for illicitly transporting and exporting sanctioned commodities to reintroduce goods into global markets, international surveillance has intensified. Consequently, regional and global players have prioritised forming stable, alternative routes that entirely circumvent sanctioned territories to mitigate the risk of exposure to secondary sanctions.

Beyond the issues with the Northern Corridor, the Europe-Asia Maritime Route’s reliability has also drastically declined amid cascading crises. Houthi attacks near Bab el-Mandeb in 2023 and 2024 caused a 45% drop in Suez traffic, but that was just the start. The current military offensive against Iran and the resulting de facto blockade of the Strait of Hormuz have exposed the true vulnerability of the global maritime architecture, leading to severe disruption to global shipping flows. With crude oil prices reaching a peak of over USD 120 per barrel at the height of the closure before partially recovering on ceasefire hopes that have since unravelled, the strait's reliability for global trade has come under increased scrutiny. Premiums for maritime war risk insurance have surged up to ten times the historical norm of 0.25% of a vessel's total insured value, further eroding shipper confidence. The situation hit a new peak on March 28, 2026, when the Houthis officially entered the conflict by launching ballistic missiles at southern Israel. A two-week ceasefire brokered by Pakistan expired on 22 April, but the strait has remained effectively closed throughout, with Iran and the US trading accusations of violations and a US naval seizure of an Iranian cargo ship deepening the impasse. A second round of talks in Islamabad remains uncertain, with Iran's Foreign Ministry signalling no plans to return to the table. The likelihood of near-term resolution is low, and the damage to market confidence already substantial.

Shifts resulting from the protracted war in Ukraine and the 2026 escalation in the Persian Gulf are felt acutely in the Caucasus. At the intersection of the EU, China, Russia, and an embattled Middle East, the region is seeing a rapid re-evaluation of the competing corridors that have long defined its geography. With global supply chains forced into a state of rerouting, the strategic question is no longer if these alternatives are viable but under what conditions, and on what timelines, the Middle Corridor, the Zangezur/TRIPP route, or the INSTC can capture a durable share of flows from the routes that once dominated the map.

However, the rise of these alternatives is not a guaranteed win for the Caucasus. The persistent danger is that several emerging corridors are being engineered to bypass the region entirely. A primary example is Iran's newly proposed Marand-Cheshmeh-Soraya line, which is designed to link Iranian networks directly to Turkey, cutting the Caucasus out of the loop. The success of such southern "bypass" routes depends on the resolution of regional conflicts and the stability of post-war governance in Tehran. Ultimately, whether the Caucasus remains a vital central node or becomes a sidelined observer will depend on how post-conflict governance in Tehran develops and whether the Caucasus can consolidate its position as a reliable, compliance-safe alternative for global shippers in the interim.

Eurasian Connectivity: Existing Routes

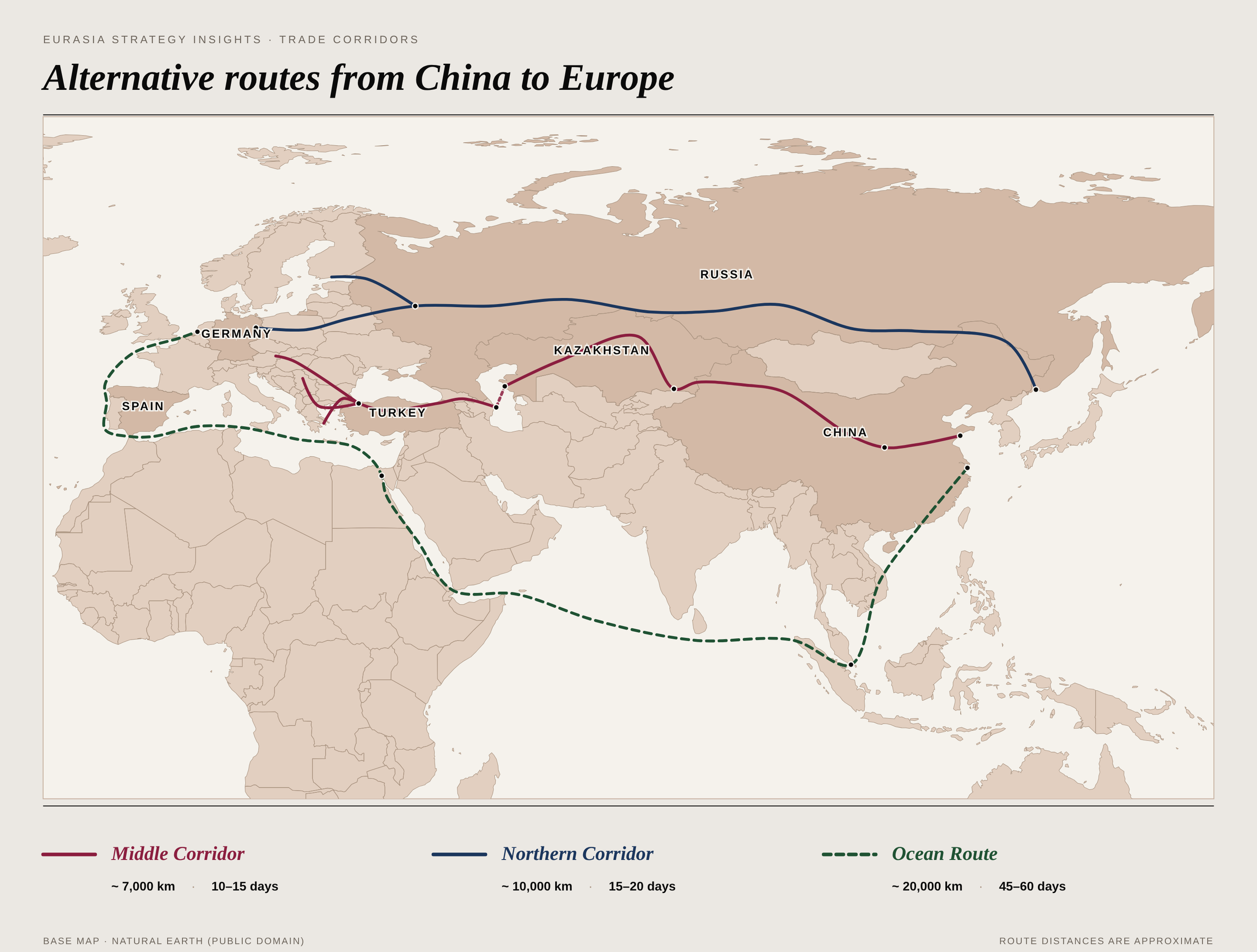

Several economic corridors currently link Europe and Asia. The most common existing routes are the Maritime Route, the Trans-Siberian Route, and the Trans-Caspian International Trade Route (also known as the Middle Corridor), alongside the emerging International North-South Transport Corridor (INSTC) and the Zangezur Corridor.

The Maritime Route

Historically, the Ocean Route has been the primary artery for Eurasian connectivity. Starting from China's eastern ports, it traverses the South China Sea and the Indian Ocean, entering the Mediterranean via the Suez Canal to reach European markets. Unlike land-based alternatives, the maritime route offers unparalleled scale and pricing flexibility; in early 2023, spot rates from Shanghai to Rotterdam hovered around USD 1,500 per 40-foot container, maintaining its status as the most cost-effective logistical choice despite a standard 45-to-60-day delivery window.

However, recent years have exposed the profound fragility inherent in this model. The COVID-19 shipping crisis and the 2021 Suez Canal blockage showed how even brief localised obstructions can trigger extensive global disruptions and multi-billion-dollar economic setbacks. This vulnerability to external factors was further evidenced following the Red Sea crisis in November 2023, when Houthi attacks near the Bab el-Mandeb Strait severely compromised maritime transit. According to the IMF, trade volumes through the Suez Canal decreased by 50 percent year-over-year in 2024, while the volume of trade forced to reroute around South Africa's Cape of Good Hope increased by an estimated 74 percent, resulting in a 10–14-day increase in shipment times. Building upon these systemic vulnerabilities, the February 2026 offensive in Iran and the de facto closure of the Strait of Hormuz have fundamentally altered the security calculus for global shipping. This escalation has materially increased the incentive for importers to diversify logistics away from traditional maritime corridors, with the reliability of the Hormuz-dependent network now a live operational risk rather than a theoretical concern. The risk is further compounded by Houthi forces joining the attacks on Israel, which raises the immediate threat of renewed blockages at the Suez Canal and Bab el-Mandeb chokepoint. These recurring disruptions, including extended detour times, inflated oil prices, and elevated insurance premiums, have materially increased the cost and risk profile of the maritime route, prompting a reassessment of long-term routing strategies among major shippers.

For the Caucasus, this instability represents a strategic turning point. While land routes cannot match the sheer volume of maritime transport, the Middle Corridor now serves as a vital risk-mitigation tool, offering operational reliability where contested maritime passages currently cannot.

The Northern Corridor

The Trans-Siberian Route, otherwise known as the Northern Corridor, originates in China and branches out into Kazakhstan or Mongolia. From there, it passes through Russia and Belarus, entering the Western European market through Poland. Alternatively, the route branches near Yekaterinburg and goes directly into the Baltic states, bypassing Belarus.

The first regular connections along the Northern Corridor were introduced in 2011, with the launch of the China-Europe Rail Express. While rail transport has historically comprised only a fraction of maritime trade, from 2011 to 2020 its share showed a positive growth trend, rising from 1% to 4% of overall trade. Over the past decade, China has heavily invested in developing the Trans-Siberian Route, leading to decreased transportation costs. For certain products, such as high-value goods, the railway is a preferable alternative to the slower maritime route. Operating via the well-established 1520mm gauge network, the Northern Corridor sustains a highly competitive transit time of 15 to 22 days from Chinese manufacturing hubs to Polish gateways like Małaszewicze. In pricing terms, the Northern Corridor sits between the cheaper maritime route and the more expensive but shorter Middle Corridor.

The resulting data reflects this volatility: between 2022 and 2023, the westbound freight volumes along the Northern Corridor plummeted by 51%. The picture in 2024 and 2025 proved more nuanced than a straightforward decline. Disruptions in the Red Sea, soaring maritime freight costs, and broader instability prompted a partial, though cautious, return to the Northern Corridor, with total China-Europe trips growing by 13% in 2024 to nearly 15,000 runs, and a significant share of this traffic still moving through Russia.

While many entities have questioned the long-term legitimacy of this route and sought to circumvent Moscow, time has demonstrated the resilience of Russia’s logistics hubs. In particular, the Middle Corridor continues to navigate its own structural reforms and overcome infrastructure bottlenecks. Yet, this operational rebound does not signal a return to the "old normal." Shippers now actively diversify their portfolios to avoid over-reliance on a single artery, while insurers apply increasingly high premiums to any Russian-linked transit.

The prospect for conflict resolution grows each year; however, in the event of a settlement, a full recovery to pre-2022 traffic levels remains unlikely, as businesses are now wary of basing supply chains on a corridor so vulnerable to geopolitical escalation. For the Caucasus, this persistence of the Northern Corridor highlights a closing competitive window.

The Middle Corridor

The Trans-Caspian International Trade Route (TITR), or the Middle Corridor, is a multimodal transport system traversing Central Asia and the Caucasus. From China, it enters Kazakhstan and moves via ferry across the Caspian Sea. After reaching Azerbaijan, cargo continues westward through Georgia into Turkey, or accesses Romanian, Bulgarian, or Ukrainian ports through the Black Sea.

The war in Ukraine led to a substantial redirection of trade from the Northern Corridor toward the Middle Corridor, establishing the route as a primary viable artery for shippers seeking to bypass Russian territories. Consequently, cargo volumes reached 4.5 million tonnes in 2024, a tenfold increase from 2021. While the development of the Middle Corridor has been met with considerable enthusiasm from Central Asian and Caucasus countries, a funding gap, unfulfilled by both European and Chinese counterparts, means the trade volume of the Middle Corridor still accounts for a fraction of the total volume passing through the Northern Corridor.

A combination of decentralised decision-making and insufficient investment underpins the Middle Corridor’s current limitations. As it stands, each transit nation independently manages its own infrastructure and customs procedures. This sovereign-led model protects the region from institutional capture, preventing global powers from using infrastructural loans to form political leverage. However, without a centralised planning body, the transit route struggles to harmonise the physical infrastructure and customs clearance.

Although the route is 3,000 km shorter than the Northern alternative and offers a theoretical transit time of just 10-15 days, it remains the most expensive land option. The transportation costs for one 40-foot equivalent unit (FEU) along the Middle Corridor range from USD 3,500 to USD 4,500, compared to USD 2,800 to USD 3,200 along the Northern Corridor. This price disparity is driven by a "five-border" clearance bottleneck, where increased border traffic and a lack of unified digital systems result in repetitive paperwork and, in practice, can extend total transit times to as much as 40 days.

In late 2025, the EU’s Global Gateway and international banks recognised the route's potential by pledging over EUR 22 billion to modernise these links. Securing capital will facilitate the deployment of a unified digital ecosystem, fully integrated with eTIR, which is the UN’s modernised, paperless global customs transit system. By synchronising distinct national systems, the Middle Corridor would improve its efficiency and cut costs.

The long-term trajectory of the Middle Corridor turns significantly on how both conflicts resolve and the degree to which successor governance in Tehran and Moscow is oriented toward compliance with international trade frameworks. The range of plausible outcomes, from full reintegration to continued sanctions exposure, carries materially different implications for operators and investors routing through the corridor. Until then, the Caucasus must prioritise resolving its internal operational frictions to capitalise on its unfolding geographic leverage. If the Middle Corridor can maintain geo-economic insulation from the surrounding regional conflicts, source additional funding and synchronise customs, the region has a narrow window to establish itself as a permanent, reliable artery rather than a temporary workaround.

Eurasian Connectivity: Routes in Development

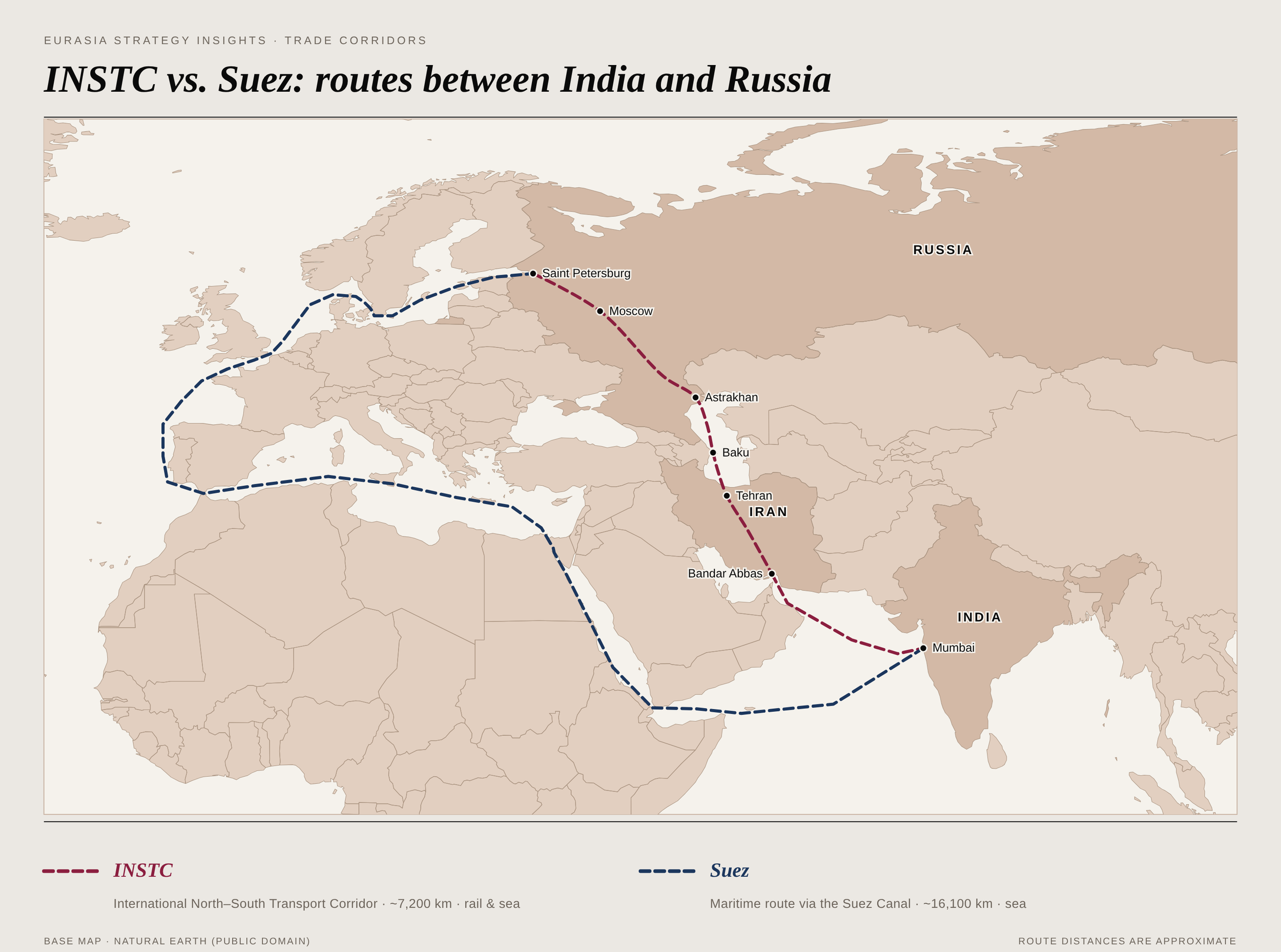

The International North-South Transport Corridor (INSTC)

The International North-South Transport Corridor (INSTC) is a multimodal network designed to link the Indian Ocean and the Persian Gulf to the Caspian Sea and onward to St. Petersburg. To achieve this, the corridor relies on three primary arteries: the Western route via Azerbaijan (with secondary flows diverting toward Georgia via the Kvesheti-Kobi road), the Trans-Caspian maritime route, and the Eastern route passing through Kazakhstan and Turkmenistan. By design, each of these branches relies on Iranian territory to access the southern ports.

The economic corridor is nearly 75% complete, but the major missing link is the Rasht-Astara railway section in Iran, an increasingly important and complex infrastructural barrier to finalising the corridor’s development.

The idea of the North-South corridor has been circulating since 2000, when Iran, Russia, and India signed a trilateral agreement. Russia and Iran had been investing heavily in modernising this infrastructure, with aims to update single-track and non-electrified railways and outdated cargo-handling equipment in the Caspian Sea. However, it was only after the 2022 invasion of Ukraine that Moscow developed a substantive interest in the INSTC as the most viable trade route free from Western political pressures. In May 2023, Russia and Iran signed a construction agreement for the project, backed by a USD 1.6 billion Russian loan, with full-scale work scheduled to begin in early 2026.

Collectively, the EU has phased out Russian oil by 92%. Meanwhile, India became Russia's most trusted partner in purchasing discounted crude. In November 2025, the U.S. placed secondary sanctions on India, putting a 50% export tariff on Indian goods, discouraging Indian export and consequently Indian businesses. However, with looming fears in supply shocks due to the blockade of the Strait of Hormuz, the U.S. Treasury recently issued a 30-day waiver easing secondary sanctions to allow India to purchase Russian oil sanction-free.

Further investments and construction plans have been indefinitely paused as the region grapples with the fallout of overlapping conflicts. Meanwhile, the Eastern branch - routing through Kazakhstan and Turkmenistan - continues to transfer a minimal flow of goods. The primary Western route through Azerbaijan and the Trans-Caspian maritime links are momentarily paralysed. Consequently, overall transit along the INSTC has plummeted to merely a fraction of its pre-2026 levels.

For Tehran, the INSTC represents a strategic opportunity to monetise its geography and circumvent its historical marginalisation in international trade. This ambition has been accelerated by a deepening bilateral alignment with Moscow, as Iran supplies drones for the war in Ukraine, and Moscow, in the meantime, has loaned USD 1.5 billion to finance the construction of Iran's segment. After peaking at 27 million tonnes in 2024, INSTC freight volumes have since come under renewed pressure amid escalating regional instability, while bilateral cargo between India and Russia had doubled during that earlier period. At peak functionality, the corridor offered a 30% cost advantage over traditional maritime routes and was projected to compress transit times from 37 days to just 19 days.

The long-term viability of the INSTC is currently suspended amid the ongoing regional escalations. Recent peace negotiations in Islamabad, Pakistan resulted in a 14-day truce, which has since hardened into a fragile ceasefire now hanging by a thread.. Simultaneously, Islamabad has signaled its commitment to the corridor's development, on April 13, dispatching its inaugural export shipment from Karachi to Tashkent. Should the conflict conclude favorably for Tehran, an emboldened Iran could solidify its standing as a legitimate partner, leveraging its position to rapidly accelerate its strategic and logistical integration between Russia and the Global South.

Independent of the ongoing hostilities, Iran's transit infrastructure has historically been characterised by deep-rooted inefficiencies. Operations are frequently disrupted by chronic domestic energy deficits and abrupt regulatory shifts, such as the sudden imposition of "Bak-e Pur" retaliatory fuel tariffs that have previously paralyzed cross-border trucking with neighboring transit states. Ultimately, while the INSTC offers a potent strategic framework for the Moscow-Tehran axis, its long-term success will require navigating both the results of two ongoing conflicts and the enduring complexities of their transit environments.

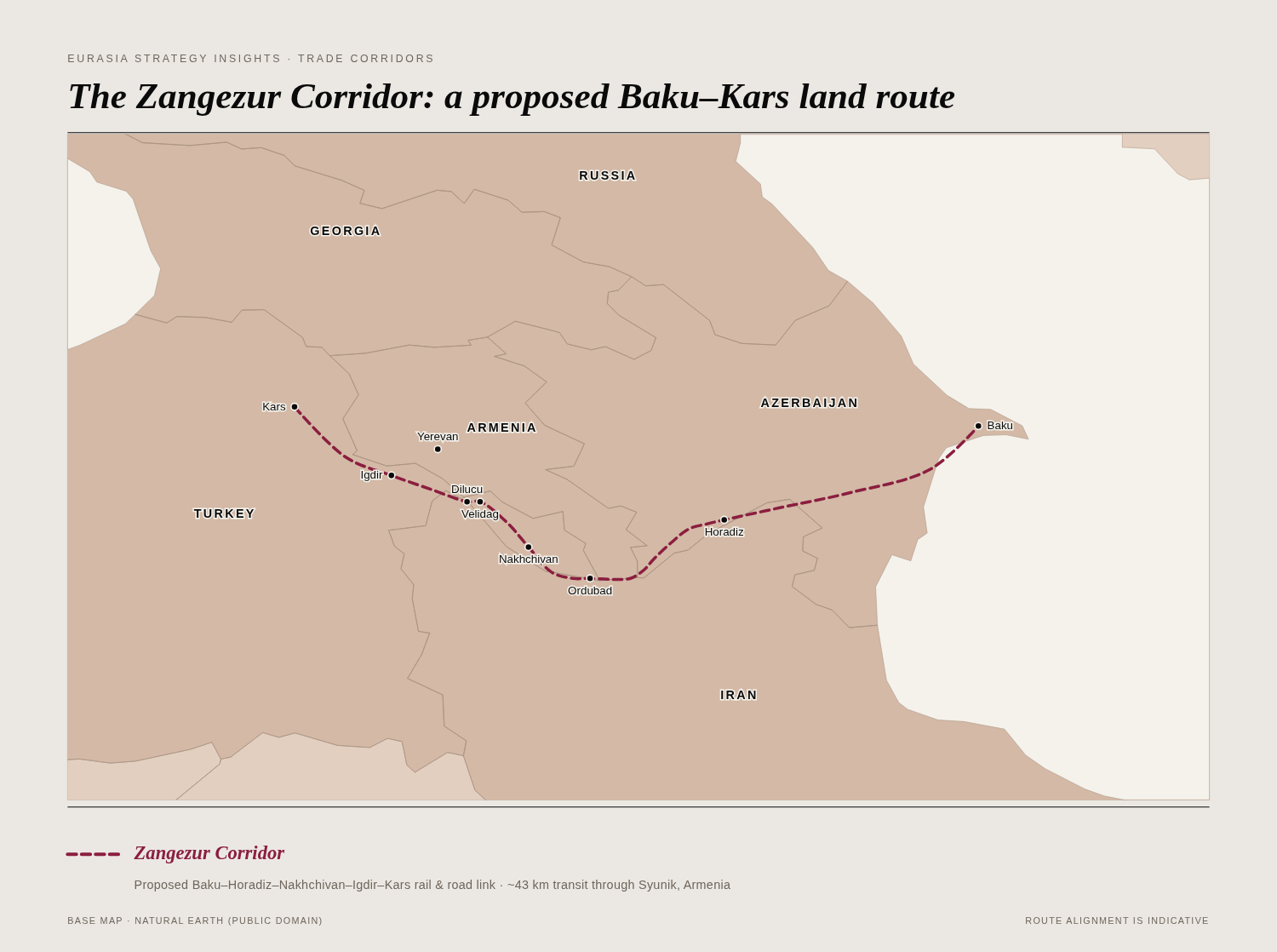

The Zangezur/TRIPP Corridor

The Zangezur Corridor, an aspirational route connecting mainland Azerbaijan to the Nakhchivan exclave through southern Armenia, has been revitalised by the recent Agreement on the Establishment of Peace and Inter-State Relations between the Republic of Azerbaijan and the Republic of Armenia. While the peace agreement marks a historic breakthrough in bilateral relations and the revised end to the 35-year conflict over Nagorno-Karabakh, it is not yet a foolproof guarantee of stability in the volatile South Caucasus region. Now rebranded as the ‘Trump Route for International Peace and Prosperity’ (TRIPP), it has reportedly been endorsed by both Nikol Pashinyan and Ilham Aliyev following negotiations in Washington, D.C., though the agreement has not yet been formally ratified. If realised, TRIPP would serve as a high-speed extension of the Middle Corridor, bypassing the traditional Georgian route in favor of a direct link between Azerbaijan and Turkey. This move aims to shave three days off the Europe-Central Asia transit, reducing the total journey time from 18 to 15 days.

Azerbaijan and Turkey had long hoped for the Zangezur corridor to materialise. On the Azerbaijani side, the 110km Horadiz-Agbend railway, linking the mainland to the Nakhchivan exclave, is nearly complete. Meanwhile, Turkey is pressing ahead with the construction of the missing segment, the 224 km Kars-Dilucu line running from Nakhchivan to Kars, with plans to finalise the entire route by 2029.

However, the corridor is far from a settled reality. While the USD 145 million in U.S. investment is a significant anchor for the Armenian rail segment, the total cost of the corridor remains largely unfunded. A central pillar of the plan is a proposed 99-year lease structure, under which Armenia grants the United States exclusive development rights over the 27-mile Zangezur Corridor. This framework allows Washington to sublease the territory to a private consortium tasked with modernising the corridor’s infrastructure, including rail, fibre optics, and energy pipelines. This legal mechanism is designed to provide the absolute long-term certainty required for such heavy capital investment by insulating the route from immediate political volatility. Yet, even this remains subject to fierce parliamentary challenges in Yerevan. Without a final, binding treaty between Baku and Yerevan, the corridor's legal status remains precarious, subject to the continued political consent of a fast-moving administration.

For Moscow, this marks a clear erosion of its traditional hegemony over East-West transit routes, coinciding with Armenia's strategic pivot toward Western security architectures. For Iran, the stakes are higher still: its narrow border with southern Armenia represents Tehran’s sole independent land corridor to Russia and European markets that bypasses Turkic-controlled territory. Should this strip transition into an internationally administered corridor, Iran risks a permanent strategic decoupling from its northern trade partners, rendering its role increasingly marginal in the revised East-West connectivity landscape. More importantly, Iran interprets Zangezur as a deeply political project that serves to strengthen the Turkey-Azerbaijan axis and fuel pan-Turkic narratives, pushing Tehran further to the margins of Eurasian connectivity.

Instead, Iran wishes to advance an alternative, the Aras Corridor, which bypasses Armenia altogether and creates a land route between mainland Azerbaijan and Nakhchivan along the Iranian border. Simultaneously, Iran is promoting a separate southern Eurasian land corridor that bypasses the Caucasus altogether. In November 2025, Iran, China, Kazakhstan, Uzbekistan, Turkmenistan, and Turkey signed a multilateral agreement in Istanbul to expand the southern route's share of container traffic, launching construction of the 200 km Marand-Cheshmeh Soraya railway.

Ultimately, much depends on Armenia's political trajectory and the nature of post-war Iranian governance. If Pashinyan stays in power and the normalisation with Azerbaijan continues, TRIPP is likely to move ahead quickly. If a Western-aligned administration takes root in post-war Tehran, Iran's southern routes could eventually rejoin the global transit architecture; until the broader regional picture stabilises, the Zangezur/TRIPP route represents the most structurally insulated option currently available, though its own realisation remains contingent on factors outside any single actor's control.

Conclusion

The Caucasus has moved from being a peripheral theatre of great-power competition to a central arena for competing connectivity strategies. The Northern Corridor, the maritime route via Suez, the Middle Corridor, INSTC, Zangezur/TRIPP, and Iran's new southern land route are not just technical options for shippers; they are competing visions of how Eurasia will be stitched together once conflict in Ukraine, Iran, and the Red Sea ceases.

For the countries across the region, newfound interconnectivity signals both an opportunity and a warning. On the one hand, instability along the Northern and maritime routes has finally pushed investors and logistics firms to take the South Caucasus seriously. On the other hand, some of the most ambitious new projects are explicitly built to bypass the region altogether. Geography still gives Armenia, Azerbaijan, and Georgia leverage, but it no longer guarantees relevance.

Whether the Caucasus becomes a backbone of Eurasian trade or a patch of transit space that others avoid will depend less on uncertain geopolitics and more on concrete policy choices. CAREC Transport Strategy 2030 already outlines a roadmap for connectivity, sustainability, multimodality, safety, and logistics efficiency. Streamlining customs, aligning regulations, reducing political risk, and avoiding zero-sum corridor competition will matter as much as building new railways or ports.

If regional actors use this moment to invest in reliability and coordination, the Middle Corridor, Zangezur/TRIPP, and the INSTC branch can anchor the Caucasus firmly into the next phase of the West-East connectivity map. If not, the 2030s may be defined by a web of southern and northern bypasses as the region watches containers move elsewhere.