Asia’s Chip Corridor

How AI demand and geopolitical competition are redrawing the global technology map

by Bree Stewart

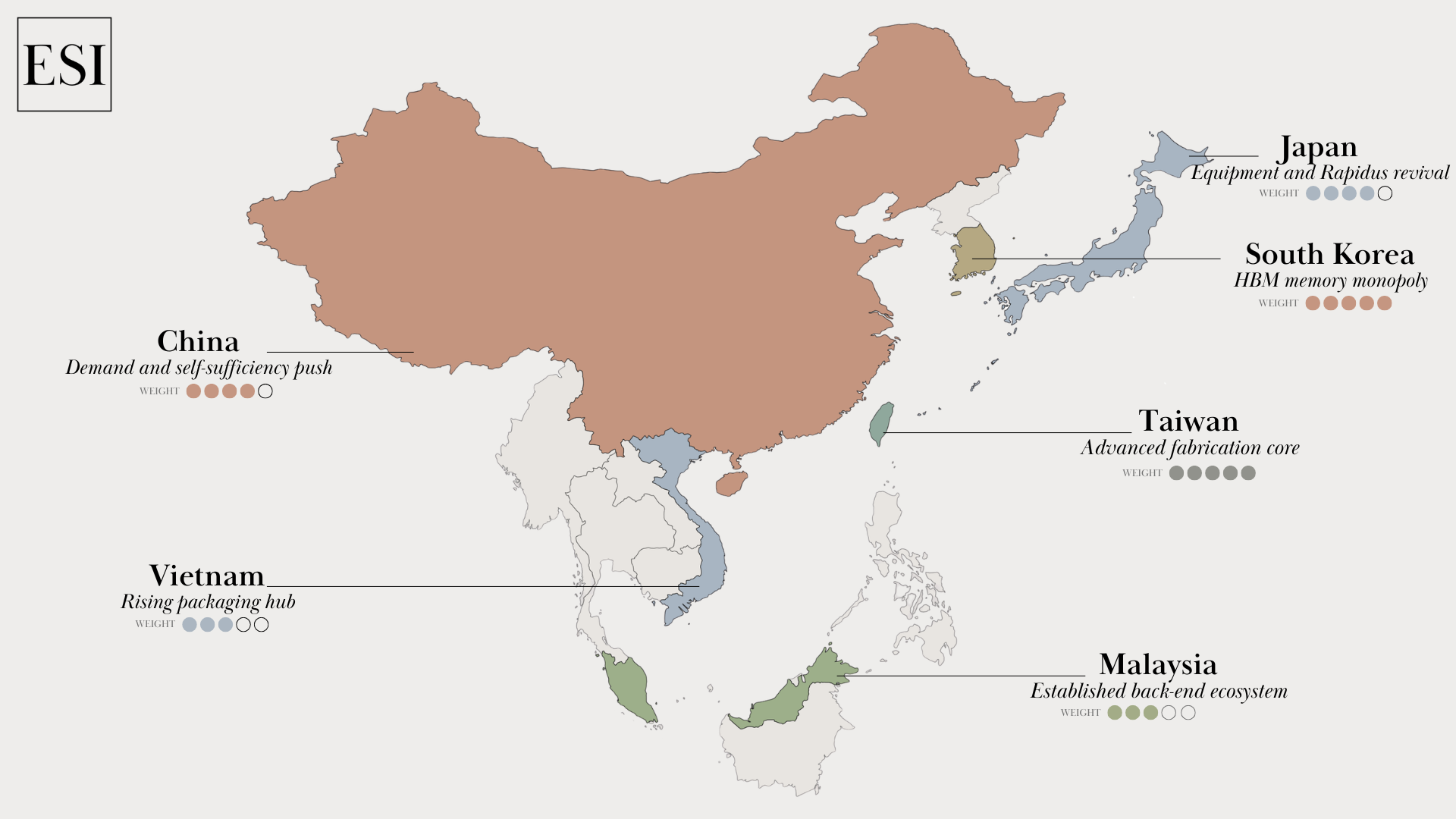

Asia's semiconductor supply chain is the backbone of the global technology economy. Over the past decade, production has shifted significantly beyond China as rising costs and geopolitical pressure have driven major technology companies to spread operations across the wider region.

Taiwan, Japan and South Korea now lead innovation and development at the frontier. In 2025, TSMC posted USD 122 billion in revenue, a 36% increase year-on-year, controlling approximately 70% of the global foundry market and over 90% of production at the most advanced nodes of 7 nanometres and below. Japan is committing tens of billions to semiconductor development, while South Korea's Samsung and SK Hynix are producing sixth-generation high-bandwidth memory chips to power AI infrastructure. Vietnam and Malaysia are expanding rapidly in packaging, testing and assembly.

The technology competition is no longer a bilateral contest between the United States and China. Nations at every level of the supply chain are making strategic bets on semiconductor development at a pace existing supply chains were not built to handle. This report breaks down the key countries, their critical dependencies and the strategic risks businesses and decision-makers should consider.

China still dominates the market

China remains the world's largest consumer of semiconductors and the largest buyer of semiconductor manufacturing equipment. In 2025, Chinese chipmakers spent approximately USD 42.75 billion on new wafer fabrication tools. China is projected to remain the world's largest equipment market through 2027, though spending is expected to ease gradually from its 2025 peak as the initial capacity build-out matures. In December 2025, Beijing introduced requirements that chipmakers use 50% domestically made equipment, a significant step in its push toward supply chain independence.

While US export controls have successfully denied China access to extreme ultraviolet lithography machines and the most advanced AI chips, they have simultaneously accelerated China’s domestic innovation effort. Beijing is supporting a rapid increase in self-sufficiency in all aspects of semiconductor design and production, with Chinese companies making notable progress in advanced packaging, alternative lithography approaches and novel systems architecture. Huawei has set a target of 70% self-sufficiency by 2028. According to the American Enterprise Institute, China's fleet of several hundred deep ultraviolet lithography machines will likely be capable of printing millions of high-end logic dies in 2026, which Huawei is expected to package into AI accelerators.

The US still dominates high-end chip design and Electronic Design Automation (EDA) software, and these advantages make it very difficult for China to produce the most advanced chips independently. Chinese semiconductor equipment companies are estimated to supply between 10% and 15% of equipment purchased within China in 2026, with production remaining predominantly concentrated at legacy nodes. ASML, the Dutch manufacturer of photolithography machines and the sole supplier of extreme ultraviolet lithography tools, remains years ahead of its Chinese counterpart Shanghai Micro Electronics Equipment.

Nevertheless, the trajectory toward greater self-sufficiency is clear and shows no sign of slowing. Beyond self-sufficiency, China is emerging as an active competitor across the corridor. Chinese firms are beginning to challenge established players in mature-node logic, advanced packaging and AI accelerator design. Huawei's Ascend chip series demonstrates that domestically produced alternatives to Western AI hardware are already reaching the market, even if they remain behind the frontier. For businesses operating anywhere in the technology supply chain, this is not simply a procurement story. It is a competitive one.

Risk analysis: The assumption that export controls will permanently constrain China’s semiconductor capabilities is becoming less tenable. Businesses should consider a scenario in which China operates an increasingly capable parallel supply chain.

Taiwan is irreplaceable

TSMC's dominance of advanced chipmaking is the most defining feature of the global technology economy. The company is responsible for the processors that power Nvidia's AI accelerators, Apple's mobile devices and AMD's data centre chips. Counterpoint Research put TSMC's share of the global foundry market at roughly 72% in the third quarter of 2025, with the company responsible for more than 90% of production at the most advanced process nodes. Samsung and Intel's foundry arms compete for what remains.

Central to Taiwan's dominance is access to equipment that almost no one else can supply. ASML, the Dutch company that manufactures extreme ultraviolet lithography machines, is the sole producer of the tools required to print the world's most advanced chips. Without ASML's machines, TSMC cannot operate at the leading edge. That single point of dependency, one company, in one country, making one category of tool, runs beneath every statistic about Taiwan's market share.

Taiwan's dominance of chipmaking comes with serious geopolitical risk. The country’s concentration of critical semiconductor infrastructure makes it a focal point of great-power competition. While there is speculation that 2027 is a likely year for Chinese military moves on Taiwan, the US Annual Threat Assessment published in March 2026 reported that Beijing has no current plan or fixed timeline. The broader international environment is nonetheless shifting in ways that matter. The war in Ukraine, the Israel-Gaza conflict and the Trump administration's stated ambitions regarding Greenland are collectively weakening the international norms that have historically constrained unilateral action. An environment with fewer constraints on great-power behaviour reduces the friction China would face if it chose to act. Any disruption to TSMC's production would be felt across every industry dependent on chips, and there is currently no other producer that can compare in terms of scale and technology.

Despite the volatile political climate, TSMC's investment trajectory shows no signs of slowing. The company is planning large volume production of 1.6nm chips by 2027 and 1.4nm chips by 2028 to 2029. TSMC has forecast capital expenditure of USD 56 billion in 2026, with revenue growth predicted at more than 30%. While TSMC's CEO C.C. Wei has acknowledged concerns about an AI demand bubble, orders from Nvidia, Apple, AMD and others continue to justify the scale of spending, underscoring how deeply the technology industry depends on Taiwan's production capabilities.

TSMC is expanding its geographical reach by building new fabrication facilities in Arizona, Germany and Japan to increase volume production and de-risk its supply chain. These investments could meaningfully improve chip access for host nations, but volume production remains years away and none of these facilities will replicate the scale of Taiwan's output in the near term. The drive to expand beyond Taiwan reflects genuine demand for a less concentrated supply chain, though sustained support from host-country governments and industry partners will be essential to maintain the momentum required to build even a comparable production line.

The geopolitical risk should not be underestimated. A conflict involving Taiwan would not only devastate chip supply directly but could also slow or reverse the diversification efforts currently under way elsewhere. Businesses and decision-makers should avoid treating these emerging facilities as a near-term solution. A slowdown in AI demand could equally affect TSMC's willingness to sustain its overseas capital commitments.

Risk analysis: There is currently no mitigation strategy of scale that could compete with Taiwan. A disruption in TSMC’s operations would severely affect the technology industry.

Japan's Path to Global Tech Leadership

Japan's reputation for hardware excellence has not translated into leadership in the cloud and AI era. A risk-averse corporate culture and a long preference for capital-intensive manufacturing over software platforms left the country trailing behind the United States and China through the 2010s. Rapidus, a semiconductor company established in 2022 with backing from Toyota, Sony, NTT, SoftBank and the Japanese government, represents the most significant attempt to return Japan to the forefront of advanced semiconductor manufacturing.

On 27 February 2026, Rapidus closed a JPY 267.6 billion (USD 1.7 billion) funding round, with the Japanese government taking 11.5% of voting rights and a golden share giving it the power to block major management decisions, according to Bloomberg and Jiji Press. Those voting rights are designed to scale up to 40% if the company's performance falters, a structure that makes Tokyo a controlling stakeholder in a national project it cannot afford to let fail.

So far the company has delivered its key milestones. Rapidus reported the first successful operation of 2nm gate-all-around transistors, developed at its IIM-1 (Innovative Integration for Manufacturing) pilot line in Chitose, Hokkaido. In April 2026, NEDO (New Energy and Industrial Technology Development Organisation), a Japanese government agency, approved Rapidus' fiscal 2026 plan, which sets out processes to release its Process Design Kit to early customers and demonstrate that its production systems can operate at the required speed. The company is targeting mass production by 2027.

Rapidus will produce far fewer chips than giants like TSMC, but this is intentional. Its selling point is speed and flexibility over volume. The company can produce chips faster and in smaller batches, which appeals to AI, defence and niche customers who want domestically produced chips quickly and are willing to pay a premium for them. According to Bloomberg, CEO Atsuyoshi Koike told reporters in February 2026 that Rapidus was in discussions with more than 60 prospective customers.

Rapidus now has 32 private investors, including Canon, Fujitsu and the Development Bank of Japan. The Japanese government has committed approximately JPY 2.35 trillion (USD 14.64 billion) to the project, with Japan's broader commitment to semiconductors and AI standing at around JPY 10 trillion (USD 65 billion) through 2030. This puts Japan alongside the United States and the European Union in the global race to build sovereign chip capacity.

The wider strategy is already in motion. TSMC is building a second factory in Kumamoto using a 3nm process, though mass production has been pushed back to 2028 due to weaker demand from the automotive industry and a shift of investment toward US fabs. Even so, it anchors another advanced chip facility on Japanese soil. Underpinning all of this is Japan's long-standing dominance in semiconductor equipment and materials, an advantage that predates the current boom and remains central to the broader revival being built around it.

The biggest risk for Rapidus is not a lack of funding or ambition, but whether it can develop chips that meet reliability and yield requirements by 2027. If the company misses its target, continued political and financial support cannot be assumed. If it succeeds, chip buyers and technology companies will have a credible third option for advanced chips beyond TSMC and Samsung. For those concerned about over-reliance on Taiwan, Rapidus would offer an alternative source particularly suited to smaller batches on short turnaround times. For defence and government buyers seeking production outside a geopolitically sensitive region, it may also present a genuinely preferable option.

Risk analysis: Japan's semiconductor revival is a long-term investment with limited near-term commercial impact. However, for organisations planning ahead, particularly those with exposure to Taiwan supply chain risk, the strategic implications for diversification are significant.

South Korea’s Memory Dominance and the AI Demand Surge

The rapid scaling of AI infrastructure has created a significant concentration of demand around high-bandwidth memory, a market dominated almost entirely by South Korea's Samsung Electronics and SK Hynix. High-bandwidth memory has become the critical enabler of AI training and inference, and South Korea controls the overwhelming majority of global supply. SK Hynix maintained a dominant position throughout 2025, holding approximately 62% of global HBM shipments in Q2 2025. Goldman Sachs predicts SK Hynix will hold over 50% of the HBM market through 2026, while UBS projects it could capture 70% of the HBM4 market for Nvidia's next-generation Rubin platform.

Both Samsung and SK Hynix began mass production of HBM4 in February 2026, ahead of schedule and driven by increasing demand from AI infrastructure producers. Samsung is expanding production capacity by around 50% in 2026, while SK Hynix has announced plans to increase capital investment by more than four times its previously stated figure. SK Hynix's M15X facility in Cheongju, backed by over 20 trillion won in investment, is set to complete its first clean room in May 2026 and will produce both HBM3E and HBM4. Bank of America estimates the HBM market will reach USD 54.6 billion in 2026, up 58% year-on-year. HBM3E prices have risen nearly 20% for 2026 deliveries as demand from Nvidia, Google and Amazon outpaces supply. With these large players all competing for the limited HBM supply, smaller buyers will need to consider hardware vendor’s memory supply chain as an important part of procurement risk management.

Both Samsung and SK Hynix began mass production of the latest generation of high-bandwidth memory, HBM4, in February 2026, earlier than originally planned. Both companies are significantly expanding production capacity to meet surging demand from AI infrastructure builders. Bank of America estimates the HBM market will reach USD 54.6 billion in 2026, up 58% year-on-year, with prices for existing HBM products rising nearly 20% for 2026 deliveries as demand from Nvidia, Google and Amazon continues to outpace supply. For smaller technology buyers outside the hyperscaler tier, this creates a real procurement challenge. Access to the memory chips needed to build or run AI systems is increasingly being shaped by the purchasing power of a handful of very large companies.

The scale of demand is illustrated by a single agreement. In October 2025, Samsung and SK Hynix signed a letter of intent with OpenAI to supply 900,000 DRAM wafers per month for the Stargate project, the joint initiative by OpenAI, SoftBank and Oracle to build AI data centre capacity across the United States. This single agreement represents a significant share of total global DRAM output and underscores how central South Korean memory producers have become to the most consequential AI programmes currently underway.

For businesses planning AI investment, the implications are practical. The cost of training and running AI models is increasingly tied to the output of just two companies in one country. Supply is constrained, prices are rising, and there are limited alternatives. Any disruption to South Korean memory production, whether geopolitical, industrial or environmental, would have immediate consequences for the global AI industry.

Risk analysis: South Korea's grip on HBM supply makes it an unavoidable dependency for any organisation building AI infrastructure. For investors, SK Hynix's HBM4 ramp and Samsung's yield progress are the key metrics to watch.

Malaysia and Vietnam: Southeast Asia’s Rising Hubs for Chip Packaging and Assembly

The back end of the semiconductor supply chain, where chips are packaged, tested and assembled into finished products, is shifting rapidly toward Southeast Asia. Malaysia is becoming an increasingly established player, responsible for approximately 13% of the global chip packaging, assembly and testing market, a sector that represents 40% of the country's total export output. In Penang, Intel's most advanced packaging complex, backed by a MYR 12 billion (Malaysian ringgit) investment, is expected to begin first-phase operations by the end of 2026. Intel has committed a further USD 208 million to its Malaysian assembly and testing operations, reinforcing its strategy to diversify advanced packaging capacity outside the United States. Infineon is investing USD 5.4 billion over five years in Malaysia, and Micron has opened its second assembly and testing plant there.

Vietnam's rise is more recent but moving quickly. Samsung is building a USD 4 billion chip packaging facility in Thai Nguyen province, bringing its total investment in Vietnam to over USD 23.2 billion. Amkor Technology is constructing its most advanced global facility, a USD 1.6 billion plant in Bac Ninh, while Hana Micron is investing around USD 930 million to expand packaging capacity. Vietnam currently accounts for roughly 1% of global semiconductor packaging and testing capacity, but Reuters projects this will rise to between 8% and 9% by the early 2030s. In 2025, Vietnam approved its first wafer fabrication plant, a signal of its intention to move beyond back-end assembly into more advanced parts of the supply chain.

As companies diversify away from China, Malaysia and Vietnam offer lower labour costs, stable policy environments and proximity to Northeast Asian design and fabrication hubs. Engineer salaries in Vietnam range from USD 10,000 to USD 15,000 compared to USD 65,000 to USD 70,000 in the United States. Malaysia offers a more mature ecosystem at similarly competitive costs.

The principal risk for both countries is workforce capacity. Vietnam has approximately 6,000 semiconductor engineers against an annual demand for 150,000 IT and digital engineers, and infrastructure constraints, particularly around power reliability, remain a concern. Major multinationals are investing heavily in both markets and government policy is actively supportive, but businesses building long-term operations here should factor investment in local training and education into their plans. First movers will have advantages in securing talent, facilities and government incentives that later entrants will find harder to replicate.

Risk analysis: Malaysia and Vietnam offer credible alternatives to China for chip packaging and assembly, but talent shortages and infrastructure constraints are real limitations. Businesses should factor these gaps into their timelines and operational planning before committing to either market.

What Comes Next: Implications for Businesses and Decision-Makers

The semiconductor corridor running from Northeast Asia through Southeast Asia is the present architecture of the global technology economy, and it is changing rapidly. Several implications follow for businesses, investors and policymakers.

Invest in supply chain visibility. Knowing your tier-one suppliers is no longer sufficient. A chip designed in California may be fabricated in Taiwan on Dutch equipment and packaged in Malaysia. Businesses that can map their exposure across at least three tiers of the semiconductor supply chain will be able to identify vulnerabilities before they become disruptions, and find alternatives before their competitors do.

Plan around diversification timelines, not headlines. The direction of travel is clear, but the destination is further off than it may appear. Rapidus, Vietnam's packaging sector and the US CHIPS Act fabs are all progressing, but volume production remains years away for most. Businesses that incorporate realistic timelines into their planning now will be better placed to capitalise on new capacity as it comes online.

China's parallel supply chain changes the competitive landscape. China is building a semiconductor ecosystem that is becoming increasingly capable, and this creates two distinct challenges. For businesses that supply equipment, software or materials to Chinese chipmakers, export controls are tightening and the rules around what can and cannot be sold are changing regularly. For businesses that compete with Chinese technology products, they face rivals with access to government subsidies, protected domestic markets and improving manufacturing capability. That competitive pressure will grow over the next five years. Businesses that map their exposure now and monitor policy developments closely will have more options and more time to adapt when the rules change again.

Southeast Asia warrants dedicated attention. The capacity being built in Malaysia and Vietnam is integral to the future chip supply chain. Penang and Bac Ninh are becoming critical nodes. Businesses that establish relationships, operations or investments in these markets now will have advantages in talent, facilities and government incentives that later entrants will find harder to secure.

Asia's semiconductor corridor is reshaping the global technology economy in ways that will be felt across every industry that depends on advanced chips. TSMC's dominance, South Korea's grip on memory, Japan's long-term revival, China's accelerating self-sufficiency and Southeast Asia's expanding role in assembly and packaging are not isolated trends. They are interconnected and will determine who gets access to the technologies that matter most over the next decade. The businesses and investors that engage seriously with these dynamics now, rather than waiting for clarity that may never fully arrive, will be better positioned to build resilient supply chains, identify emerging opportunities and make decisions that hold up as conditions continue to evolve.